Wage Growth and Inflation in Europe: A Puzzle?

Raju Huidrom, Petia Topalova, and Richard Varghese, International Monetary Fund

Does wage increase fuel inflation? While this wage-price linkage has long been at the heart of macroeconomic analysis, it appears to have waned in recent years. Specifically, over the last few years, until the outbreak of the COVID19 pandemic, wages were rising faster than productivity in many advanced economies. We would have expected this to lead to inflation pressures, yet signs of underlying consumer price pressures remained limited. This was especially the case in Europe where wage growth – adjusted for productivity – exceeded inflation during 2017-19. Economic theory suggests that if real wage growth exceeds productivity gains, the higher labor costs faced by businesses should eventually raise the prices of the products and services they provide. The apparent disconnect between wage and price developments in the last few years is thus puzzling. To shed light on this puzzle, in recent research (Boranova et al. 2019), we examine the link between wage growth and inflation using a sample of 27 European countries over 1995-2019. While our research focuses on Europe, the forces that we consider apply more broadly, and our findings are informative also for non-European countries.

Weaker passthrough from wage growth to inflation in recent years

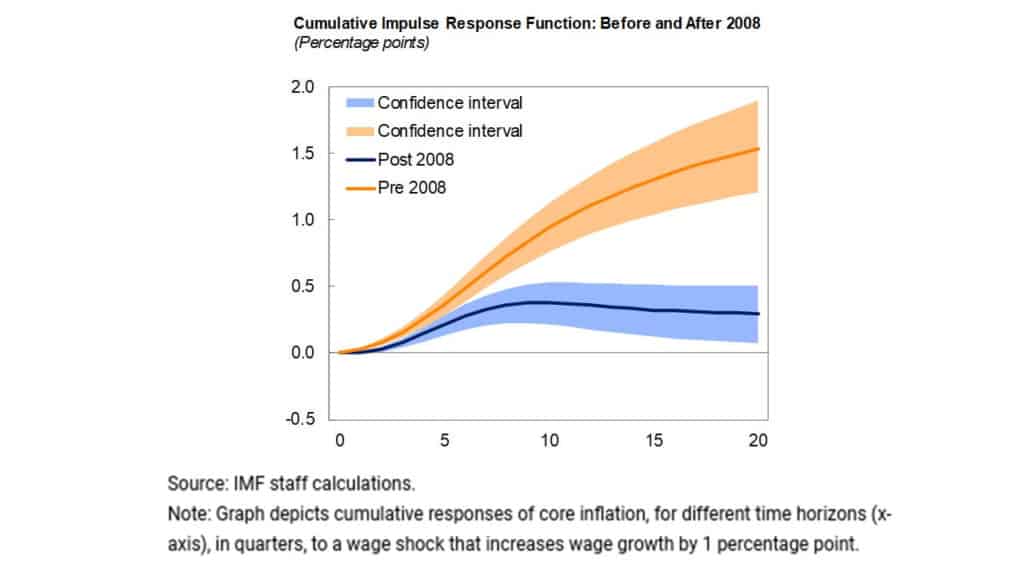

We assess the transmission of shocks to wages into prices using a panel vector autoregression (PVAR) analysis. Our results show that, historically wage growth has led to higher core inflation, as shown by the orange line in the figure below. The impact of a wage shock on inflation is rather small initially, but builds up over time, peaking around six quarters before slowly dissipating. The passthrough–defined as the ratio of the cumulative change in inflation at the end of three years to the respective cumulative change in wage growth–is about one-third.

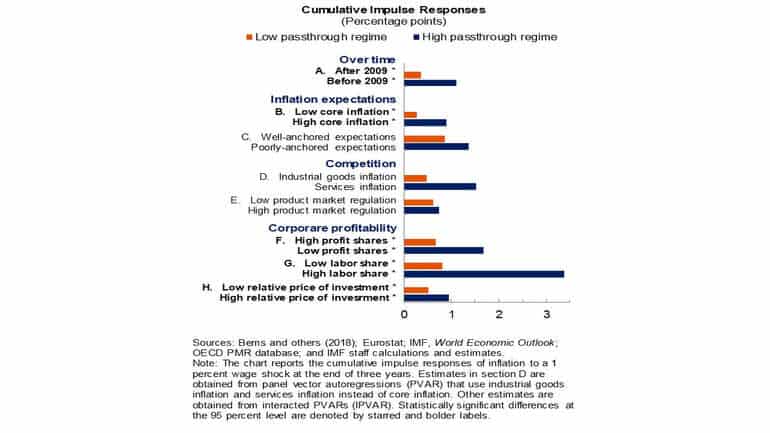

However, the passthrough of labor costs to inflation has weakened since 2008, as shown by the blue line. Our analysis using an interacted panel vector autoregression (IPVAR) framework suggests that since the global financial crisis the passthrough is one-third weaker than it was beforehand. We examine three factors that could explain this observation–the role of inflation and inflation expectations, domestic and foreign competition, and corporate profitability. The results of our analysis are summarized in panels A-H in the figure below that presents the extent to which wage shocks are transmitted to prices. Panel A indicates that this passthrough has decreased since 2009, as pointed above.

Expectations of low inflation

In a world where persistently low inflation feeds into lower expectations of future inflation, the price-setting behavior of firms might have changed. If firms expect low inflation, they may be reluctant to pass higher labor costs onto consumers since they expect their competitors to hike their prices only moderately. Thus, price stability, for example due to improved inflation expectations anchoring, is likely to reduce the sensitivity of inflation to wage growth. We examine this stylized narrative using two complementary exercises. First, we test whether the link between wage growth and inflation depends on the prevailing inflation rate in the economy. While a crude proxy of inflation expectations, this analysis allows us to overcome data limitations inherent in the second approach where we directly examine the role of inflation expectations anchoring as measured in Bems et al. (2018). Both of these exercises confirm our prior—the passthrough from wage growth to inflation is lower in a low-inflation environment (panel B) or when inflation expectations are firmly anchored (panel C).

Rising competitive pressures

We formally examine the role of competition by decomposing aggregate price into goods and services prices, and analyzing how the wage passthrough differs across goods and services. Why does this matter for the competition channel we propose? Import penetration—a proxy for foreign competition—is around 60 percent in the manufacturing sector but less than 5 percent in services. We find that the passthrough from wages to prices is stronger for services as opposed to industrial goods (panel D). This is consistent with the idea that higher exposure to competition leads to a lower passthrough from wage growth to inflation. A complementary exercise using more granular sectoral data confirms that higher exposure to foreign competition is directly associated with lower growth in producer prices. Finally, we find that the passthrough of wage growth to inflation is marginally higher in countries with higher domestic regulatory barriers in product markets, and hence lower domestic competition (panel E).

Comfortable profit margins

The analysis on the role of competition leads us to ask how firms might absorb wage growth without passing them on to price increases. We start by examining the role of an obvious candidate—corporate profitability. To the extent that firms have comfortable profit margins they may be able to absorb higher wage costs without increasing prices. We find some support for this line of reasoning. When the economy-wide corporate sector profit share is relatively high, a significantly smaller share of wage growth finds its way into consumer prices inflation (panel F). Labor share of income, which mirrors corporate profitability, too affects the passthrough—low labor share implies wage developments matter less for inflation (panel G). Our analysis regarding the role of competition and corporate profitability when taken together, however, may seem incompatible. But this is not necessarily so. Many factors—cheaper intermediate inputs, lower taxation, or financing costs, and new technologies—may support corporate profitability in the face of increased competition even as wages rise. Indeed, we find the passthrough from wages to inflation to be lower during times of low relative prices for machinery and equipment (panel H).

All these factors that we discuss as determinants of the post-crisis decline in the passthrough suggest that robust wage growth, prior to the outbreak of the COVID19 pandemic, likely had a muted effect on inflation.

The views expressed herein are those of the authors and should not be attributed to the IMF, its Executive Board, or its management.

References

Bems, Rudolfs, Francesca Caselli, Francesco Grigoli, Bertrand Gruss, and Weicheng Lian. 2018. “Expectations’ Anchoring and Inflation Persistence”. IMF Working Paper 18/280, International Monetary Fund, Washington, DC.

Bobeica, Elena, Matteo Ciccarelli, and Isabel Vansteenkiste. 2019. “The Link between Labor Cost and Price Inflation in the Euro Area.” ECB Working Paper No. 2235, European Central Bank, Frankfurt am Main.

Boranova, Vizhdan, Raju Huidrom, Sylwia Nowak, Petia Topalova, Volodymyr Tulin, and Richard Varghese. 2019. “Wage Growth and Inflation in Europe: A Puzzle?” IMF Working Paper No. 19/280.