A tale of two shocks: financial stress and sovereign default risk during the Covid19 crisis

Caterina Rho, Economist at the DG Financial Stability of Banco de México

The Covid19 pandemic is causing unprecedented stress on public finances. The virus is simultaneously hitting financial markets and the real economy, with potential disruptive effects on public finances in advanced (AEs) and especially emerging market economies (EMs). The health emergency called for sudden increases in fiscal spending, not only to assure adequate hospital care and protection to medical practitioners and coronavirus patients, but also to fund exceptional unemployment insurance programs and emergency support to the private sector, especially strategic firms and small and medium-sized enterprises. Higher public spending, combined with lower fiscal revenues as well as contracting GDP, is leading to increases in the government debt-to-GDP ratio, calling into question the sustainability of the current fiscal stance. At the same time, the increase in uncertainty due to the effects of the virus and the duration of the epidemics hit financial markets. This caused a drop in stock market prices and a sudden stop in capital flows to EMs, with negative effects on domestic currencies, inflation expectations and balance sheets.

The contemporaneous impact of the Covid19 outbreak on the real economy and financial markets is significantly increasing the risk of sovereign default in many EMs. Financial stress can amplify the impact of fiscal vulnerabilities and deteriorating economic fundamentals on the probability of sovereign default through a variety of channels. First, financial stress may weaken markets’ ability to finance sovereign liabilities to the extent that it impacts risk appetite and market liquidity. Second, financial stress can act as a wake-up call that induces complacent or inattentive investors to pay more attention to hitherto-ignored weak fundamentals. Third, financial stress can shed new information on a country’s contingent liabilities that might inflate future public debt. To the extent that the impact of public debt on sovereign risk is non-linear and increasing, information on future upsurges of public debt should have a bigger impact on sovereign risk, the higher the level of current debt.

In a recent paper with Manrique Saenz (Rho and Saenz, 2020) I analyze how financial stress amplifies the negative effects of fragile macroeconomic fundamentals on the probability of sovereign default, a risk that may be underestimated in normal times. This is relevant in the context of the Covid19 crisis, where a contemporaneous negative shock increased both financial stress and the fragility of the real economy. We use a panel dataset of debt burden indicators, sovereign spreads and sovereign defaults that covers 113 Market Access countries, including AEs and EMs, over the period 1990-2014.

We consider two measures of sovereign risk: (i) the country’s 10-year sovereign bond spread with respect to the US-Treasury bond and (ii) the probability of sovereign default. The first measure has the advantage of capturing increases in vulnerabilities even when these are not big enough as to lead to sovereign default. We use an OLS model to estimate the impact of fiscal vulnerabilities on sovereign bond spreads in AEs and EMs and whether such impact is amplified during times of distress in financial markets. Our second measure of sovereign risk is estimated using a logit model based on a dummy for sovereign default episodes. This estimation applies only to EMs given the lack of sovereign default episodes among AEs.

Financial stress can originate from domestic or foreign causes, and we therefore, use two different indicators of private financial stress, a local one and a global one. The local stress indicator is the time series of systemic banking crises estimated by Laeven and Valencia (2018). We consider two alternative measures for the global indicator. The first is a dummy based on the growth rate of the broker-dealer leverage. The second is a dummy that signals excessive increases (higher than 2 standard deviations from the mean) in the VIX index.

We find that sovereign spreads increase with public debt, higher inflation and exchange rate overvaluation, but decrease with higher real GDP growth, GDP per capita, and global growth. We also find that at times of financial distress, the impact of public debt on sovereign spreads is significantly amplified. At times of local financial distress, the impact of other economic fundamentals on sovereign spreads is also amplified: GDP per capita and the level of international reserves (in percent of GDP) seem to matter significantly more for sovereign risk at times of local financial distress than during tranquil times.

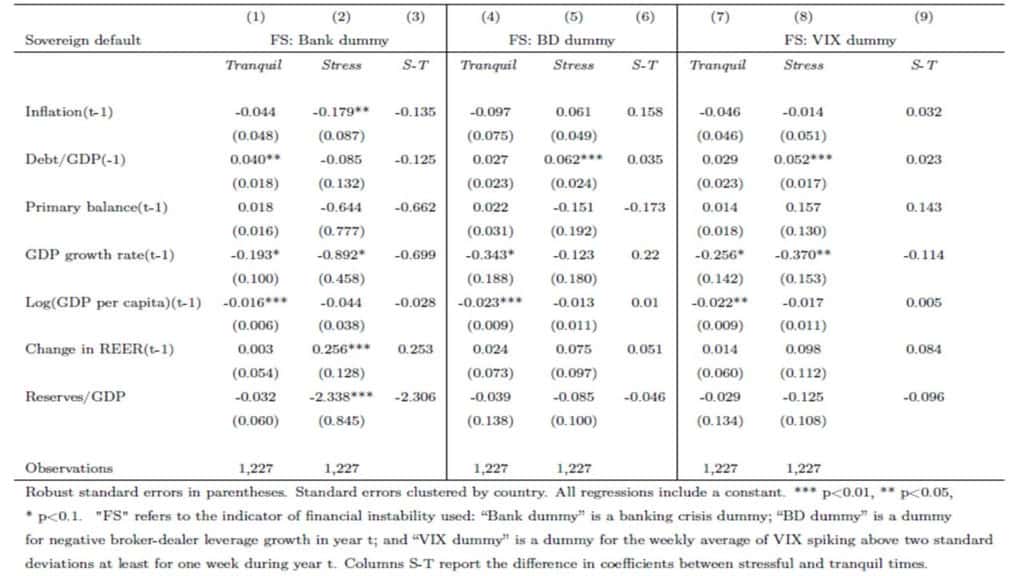

Table 1: Average marginal effects of the macroeconomic indicators during tranquil and financial stress periods (Logit model, Emerging markets, 1990-2014)

Table 1 presents the average marginal effects of our set of macroeconomic indicators on the probability of sovereign default in EMs, computed with the logit model. Columns (1) to (3) consider financial stress driven by a local shock, while columns from (4) to (9) consider financial stress from a global financial shock. Public debt is found to impact the probability of default of EMs, and its impact is also amplified significantly during periods of global financial stress. International currency reserves are found to mitigate the probability of default, particularly during times of local financial stress. Finally, a drop in GDP growth rate during times of local or global financial stress is also worsening the sustainability of sovereign debt. We can interpret the Covid19 pandemic as an exogenous global shock that increases financial stress in EMs. Our empirical results justify the current concern for sovereign debt sustainability in those markets.

References

Laeven, Luc and Fabian Valencia (2018). “Systemic Banking Crises Revisited”. IMF Working Paper 18/206, September

Rho, Caterina and Manrique, Saenz, (2020). “Financial Stress and the Probability of Sovereign Default”, submitted.

https://caterinarho.wixsite.com/home/research